On 9th March 2024 HBF Chair, Sean Trivass, emailed the Gambling Commission asking for an update on the organisation’s position on the Protection of Customer Funds. The following response has been received:

On 14 Mar 2024, at 12:04,

Dear Sean

Thank you for your email on 9 March.

You have asked if we can confirm the Commission’s position in relation to the protection of customer funds. You say that you still find it unacceptable that a ‘not protected’ rating is permitted and hoped that we may feel the same.

Our long-standing approach to customer funds recognises that the gambling sector is not equivalent to other sectors where high levels of protection may be required due to the high value of funds held and the potential impact that a loss of these funds could have on customers (such as pensions and private bank accounts). This is why we do not require gambling licensees to have a mandatory level of protection. We have always adopted a transparency and buyer beware approach for funds held with gambling licensees and have placed no specific burden on gambling licensees to protect customer funds in the case of insolvency.

We do require remote and non-remote gambling licensees to be transparent about whether, and if so how, those monies are protected. For example, gambling licensees’ terms and conditions must include information about their arrangements for protecting the customer funds they hold in the event of insolvency, the level of that protection and the method by which it is achieved. They must make this information available at the point at which a customer first deposits money, in a manner which requires customers to actively acknowledge that they have received it. They must not allow customers to use their funds for gambling until they have received an acknowledgement from the customer.

Gambling licensees must disclose to customers any changes to their arrangements for protecting customer funds and require an acknowledgement from the customer before allowing the customer to gamble with funds deposited after the change (Licence Condition 4.2.1).

In 2022, we explored the status of customer funds protection via a gambling licensee data request as to the level of protection held by remote gambling licensees, and the range of customer funds held. Out of a sample of 118, just over half of the 113 gambling licensees who responded to the data request reported that they had a level of protection for customer funds in the event of insolvency. Of those that had no protection, the majority were smaller gambling licensees, who reported that they did not have many customers (who did not have large amounts of money held by the gambling licensee). This suggests that overall, the risk to customer funds in the event of gambling licensee insolvency should be relatively low (only 3 percent of funds were unprotected). However, there are some customers who had large balances held by gambling licensees with no protection.

In November 2023, we published a consultation on proposed changes to the Licence Conditions and Codes of Practice (LCCP) for a number of topics, including the protection of customer funds. This did not propose that the ‘not protected’ rating be reviewed. As our focus is on consumer knowledge and awareness, we proposed that gambling licensees with a ‘not protected’ rating add additional customer warning messages beyond those already required. These additional messages would follow a similar process to that currently required for initial deposit and on the first deposit post a change in protection levels.

We proposed two options – option A makes the additional warning messages subject to the value of funds reaching a threshold amount, and option B would not include a threshold. Both options would require a reminder to be sent to the customer no more than once every six months. These options give customers the opportunity to choose to remove their funds from the gambling licensee if they decide that they are no longer content with such arrangements.

We consider the overall approach that we proposed to be proportionate to the level of risk highlighted by our 2022 gambling licensee data request. As mentioned above, this showed that only 3 percent of customer funds were unprotected. This did not, in our view, justify the regulatory burden of introducing a mandatory level of protection for all gambling licensees. However, 3 percent of customer funds amounted to £21.4m across nine million customers*. This is why we considered that there was value to consumers in proposing additional warning messages to ensure that gambling is conducted in a fair and open way.

The consultation closed on 21 February 2024. We are in the process of analysing the responses and expect to publish the Commission’s response to the consultation later this year.

As such, the Commission’s position is that we currently consider the ‘no protection’ rating to be acceptable. I appreciate this may not be the outcome that you are seeking, but I hope this email has helped to explain the rationale behind the system currently in place.

Kind regards

Gambling Commission

The HBF emphatically disagrees with this position. Bettors are strongly advised to be wary in the absence of the desired regulation.

HBF Register of Protection of Funds

In accordance with point 1 in the December 2017 version of the Betting Charter – “Advanced protection of punters’ funds” – HBF has established a Register of the degree of protection of funds being claimed by various betting companies.

Details of the Gambling Commission’s categorisation in this area are given on that organisation’s website: https://www.gamblingcommission.gov.uk/guidance/customer-funds-segregation-disclosure-to-customers-and-reporting/the-customer-funds-insolvency-ratings-system. The summary of those categories may be found below.

It should be noted that the Gambling Commission leaves it to the companies in question to decide which category they fall into, but that they may check the accuracy of this self-assessment.

Customers are advised to read the relevant T&Cs and satisfy themselves that the company in question is providing the level of service it claims.

HBF conducted an audit of a number of the more prominent betting organisations and the level of protection they claim. In the absence of any indication to the contrary, HBF has reported that self-assessment.

In the Charter, HBF asked that companies offer “medium” or “high” protection of customer funds. It has indicated where that has been claimed, and where it has not, in the accompanying Register.

Companies which do not feature on the Register are invited to contact HBF at comments@ukhbf.org if they seek inclusion. Companies which alter their level of protection are also invited to contact HBF with that information.

All details are, to HBF’s best knowledge, correct at the date of audit. HBF cannot be held liable for any errors, or for updates which occur subsequent to the date of audit.

HBF hopes to expand this Register in time and to revisit the details in it on occasion.

Updated June 2025

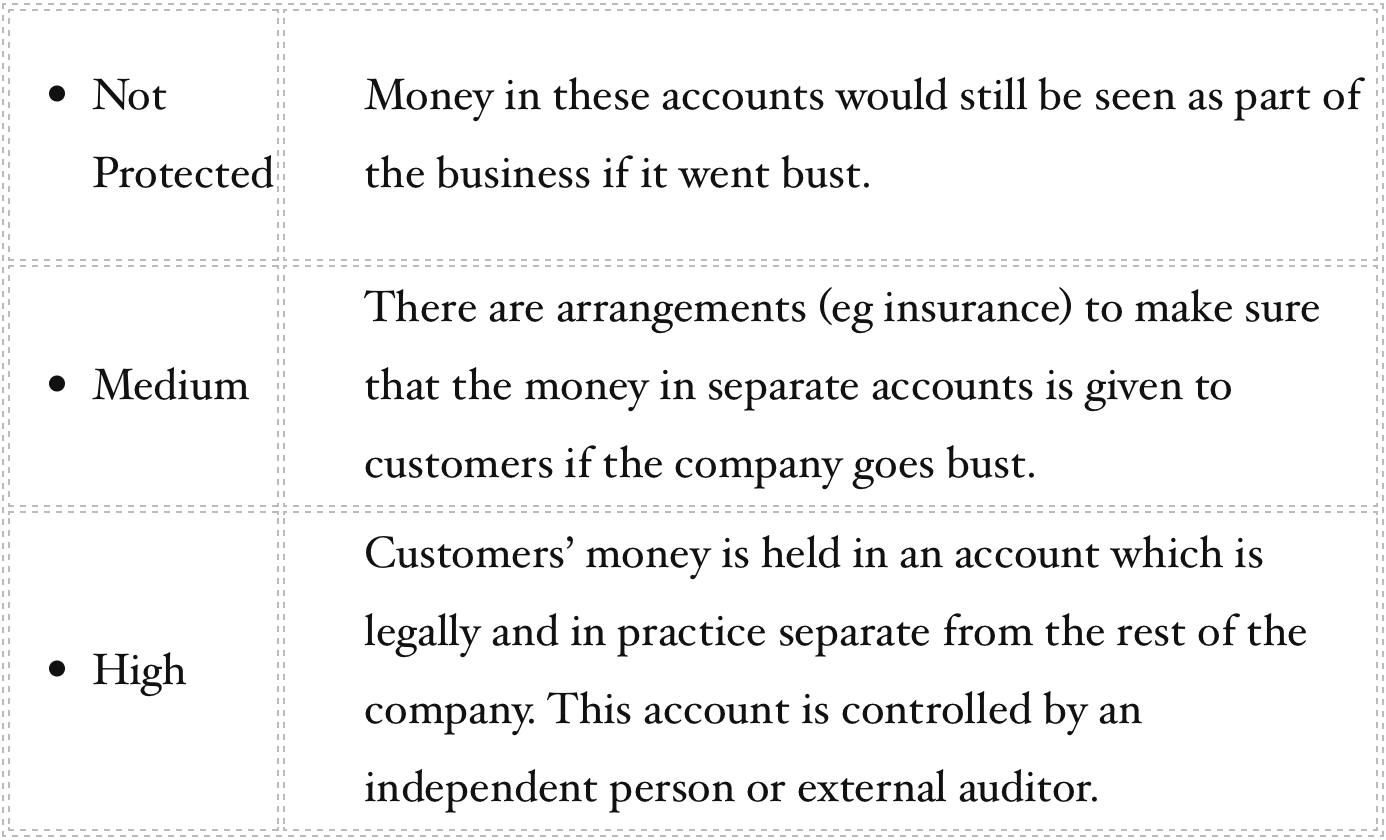

THE THREE LEVELS OF PROTECTION

N.B. All information is as reported on that company’s website at the date of audit. HBF cannot be held liable for errors, or for updates subsequent to the date of audit. Any such should be drawn to HBF’s attention. ‘Medium’ in red font denotes that these bookmakers state in their T&Cs that they cannot absolutely guarantee that all funds will be repaid.

| Date Updated | Bookmaker | Protection Level | Terms And Conditions Link | Section Where Appropriate | Maximum Payout Limit (UK racing only) | |

|---|---|---|---|---|---|---|

| 15/2/2025 | Betano | High | https://tinyurl.com/ysd3pkth | £100,000 | ||

| 15/2/2025 | Betfair Exchange | High | https://tinyurl.com/mks45efx | N/A | ||

| 15/2/2025 | Betfair Sportsbook | High | https://tinyurl.com/mks45efx | Class 1&2 £1,000,000 C 3&4 £ £250,000 C 5,6,7 £ £100,000 | ||

| 15/2/2025 | Bet Victor | High | https://tinyurl.com/3ajnxaw7 | see 10.3 | £250,000 | |

| 15/2/2025 | BetWay | High | https://tinyurl.com/326m2z69 | see 1.3 | £500,000 | |

| 15/2/2025 | BWin | High | https://tinyurl.com/3rat8k8t | see 9.17 | £1,000,000 | |

| 15/2/2025 | Coral | High | https://tinyurl.com/2uzdsr2j | see 6.10 | £1,000,000 | |

| 15/2/2025 | Ladbrokes | High | https://tinyurl.com/2tut44ry | see 9.17 | £1,000,000 | |

| 15/2/2025 | Matchbook | High | https://tinyurl.com/2s4bx74m | see 2 | N/A | |

| 15/2/2025 | Paddy Power | High | https://tinyurl.com/4z4bfs8h | Class 1&2 £1,000,000 C 3&4 £ £250,000 C 5,6,7 £ £100,000 | ||

| 15/2/2025 | Parimatch | High | https://tinyurl.com/ythyfan5 | see 10.3 | £100,000 | |

| 15/2/2025 | Pokerstars | High | https://tinyurl.com/6hwyfv8c | £50,000 | ||

| 15/2/2025 | Smarkets | High | https://tinyurl.com/sfva647a | N/A | ||

| 15/2/2025 | Sportingbet | High | https://tinyurl.com/5eu8z6ua | see 9.17 | £250,000 per week, £7,000 per bet. | |

| 15/2/2025 | 10Bet | Medium | https://tinyurl.com/3jbn75y9 | see 2 | £100,000 | |

| 15/2/2025 | 32Red | Medium | https://tinyurl.com/y4eskuf4 | see 31.2 | £250,000 | |

| 15/2/2025 | Bet365 | Medium | https://tinyurl.com/36ajassb | see 10.5 | £1,000,000 | |

| 15/2/2025 | Bet600 | Medium | https://tinyurl.com/346ppsf4 | see 1.35 | £25,000 | |

| 15/2/2025 | Bet Connect | Medium | https://tinyurl.com/bdek5rbn | N/A | ||

| 15/2/2025 | Betdaq Exchange | Medium | https://tinyurl.com/4c544axc | N/A | ||

| 15/2/2025 | BetRegal | Medium | https://tinyurl.com/35xdfe96 | see 4.4 | £90,000 | |

| 15/2/2025 | BetUK | Medium | https://tinyurl.com/sx3dtesa | see 9.11 | £200,000 | |

| 15/2/2025 | Boylesports | Medium | https://tinyurl.com/4mzjhc37 | see D1.2 | £1,000,000 | |

| 15/2/2025 | CopyBet | Medium | https://tinyurl.com/bdnhdpzu | see 34.1 | £100,000 or 1000/1 | |

| 15/2/2025 | Dafabet | Medium | https://tinyurl.com/2pwxfbv5 | see 10.2 | £50,000 | |

| 15/2/2025 | Genting Bet | Medium | https://tinyurl.com/36kd6e9n | see 33.1 | Unknown | |

| 15/2/2025 | Livescorebet | Medium | https://tinyurl.com/t4jv32km | £1,000,000 | ||

| 15/2/2025 | Leo Vegas | Medium | https://tinyurl.com/3ebvyp5r | see 9.11 | Limits mentioned but no figures quoted | |

| 15/2/2025 | Netbet | Medium | https://tinyurl.com/zjfrzja5 | see 10.3 | £20,000 per 24 hours, £50,000 per week 00.01 Monday to Sunday Midnight | |

| 15/2/2025 | Sky Bet | Medium | https://tinyurl.com/y5ynrmy4 | £500,000 | ||

| 15/2/2025 | Spreadex | Medium | https://tinyurl.com/y38nchaj | £250,000 | ||

| 15/2/2025 | Unibet | Medium | https://tinyurl.com/2vpexv2u | see 32.2 | £100,000 | |

| 15/2/2025 | Vbet | Medium | https://tinyurl.com/yj5mn6a8 | see 10.2 | £50,000 | |

| 15/2/2025 | 888sport | Medium | https://tinyurl.com/3upft45m | see 10.7 | £100,000 | |

| 15/2/2025 | Grosvenor | Medium | https://tinyurl.com/yvc974ue | see 14.4 | £250,000 | |

| 15/2/2025 | Kwiff | Medium | https://tinyurl.com/yckez2n4 | see C2.3 | £50,000 | |

| 15/2/2025 | Mr Play | Medium | https://tinyurl.com/44umdde9 | see Terms 4.4 | £90,000 per bet AND per month | |

| 15/2/2025 | Quinnbet | Medium | https://tinyurl.com/wx9xdjhe | see 4.14 | £250,000 but £5000 for SP bets and only £150 for Best Odds Guaranteed | |

| 15/2/2025 | The Pools | Medium | https://tinyurl.com/yh3xdzse | see Terms 4.10 | Unknown | |

| 15/2/2025 | Virgin Bet | Medium | https://tinyurl.com/448e3y4b | £1,000,000 | ||

| 15/2/2025 | William Hill | Medium | https://tinyurl.com/yc6emhmk | see 5.10 | £1,000,000 | |

| 15/2/2025 | Tote | Medium | https://tinyurl.com/33cf9733 | £250,000 | ||

| 15/2/2025 | BetMGM | Medium | https://tinyurl.com/yc2nm5xd | see 9.11 | Limits mentioned - but no figures | |

| 15/2/2025 | Bzeebet | Medium | https://tinyurl.com/khk99nk5 | see 4.4 | Limits mentioned - but no figures | |

| 15/2/2025 | Midnitr | Medium | https://tinyurl.com/yde6s36v | see 3.2.3 | £100,000 | |

| 11/2/2026 | Betfred | Medium | https://tinyurl.com/5fztyez5 | see 16.2 | £1,000,000 | |

| 15/2/2025 | Betgoodwin | Not Protected | https://tinyurl.com/4tkswc6h | see 1.36 | £100,000 | |

| 15/2/2025 | Geoff Banks | Not Protected | https://tinyurl.com/yfvn5uzu | see 6.15 | £100,000 | |

| 15/2/2025 | Karamba | Not Protected | https://tinyurl.com/yyhskvux | see 7.1 | Unknown | |

| 15/2/2025 | McBookie | Not Protected | https://tinyurl.com/2ws5fsw5 | see 28 | £100,000 | |

| 15/2/2025 | Star Sports | Not Protected | https://tinyurl.com/y8n2jfmc | see 28 | £200,000 | |

| 15/2/2025 | Planet Sport Bet | Not Protected | https://tinyurl.com/bdzkp7na | see 28 | £100,000 | |

| 15/2/2025 | Rhino Bet | Not Protected | https://tinyurl.com/ywardhwx | see 28 | £100,000 | |

| 15/2/2025 | PricedUp | Not Protected | https://tinyurl.com/35udw254 | see 28 | £100,000 | |